Wrapped

Like everyone else, I have had a lot of…let’s call it emotions in 2025. As a financial professional, the overwhelming emotion for me this year has been a feeling of cognitive dissonance. Democracy is crumbling at our feet (literally, in the case of the East Wing) and yet here I am talking about whether you should do a Roth conversion. It’s well-nigh impossible to keep focus on the minutiae of financial planning (or any other worthy endeavor) in the context of ICE raids, crony capitalism, resurgent racism, and growing attacks on ethnic and religious minorities. (Oh, and did you hear that formaldehyde is back in vogue?)

How can you think about money at a time like this?

Here’s how…

Invest your values. Earlier this year I read that money flowing into ESG funds had slowed in 2025, as socially responsible (or as I prefer, socially aware) investing has come under attack by the current Administration. Funny enough, I have only seen an increase in the number of people interested in finding simple, low fee investment options that avoid industries such as private prisons and gun manufacturers, or specific companies that have ties to the Administration. (I’m looking at you, Tesla.) I doubt that few, if any, believe that their divestment will change the behavior of these industries. It’s more about the emotional payoff that comes from exerting some measure of control during a time when so much seems to be out of your hands. The good news is that the idea that investing your values means accepting a lower rate of return just isn’t borne out by the evidence.

Check your current mutual fund/ETF holdings using screening tools such as Prison Free Funds, Weapons Free Funds, Gun Free Funds and Fossil Free Funds. If you don’t like what you see, make your next step reading this short primer I wrote earlier this year on ESG investing.

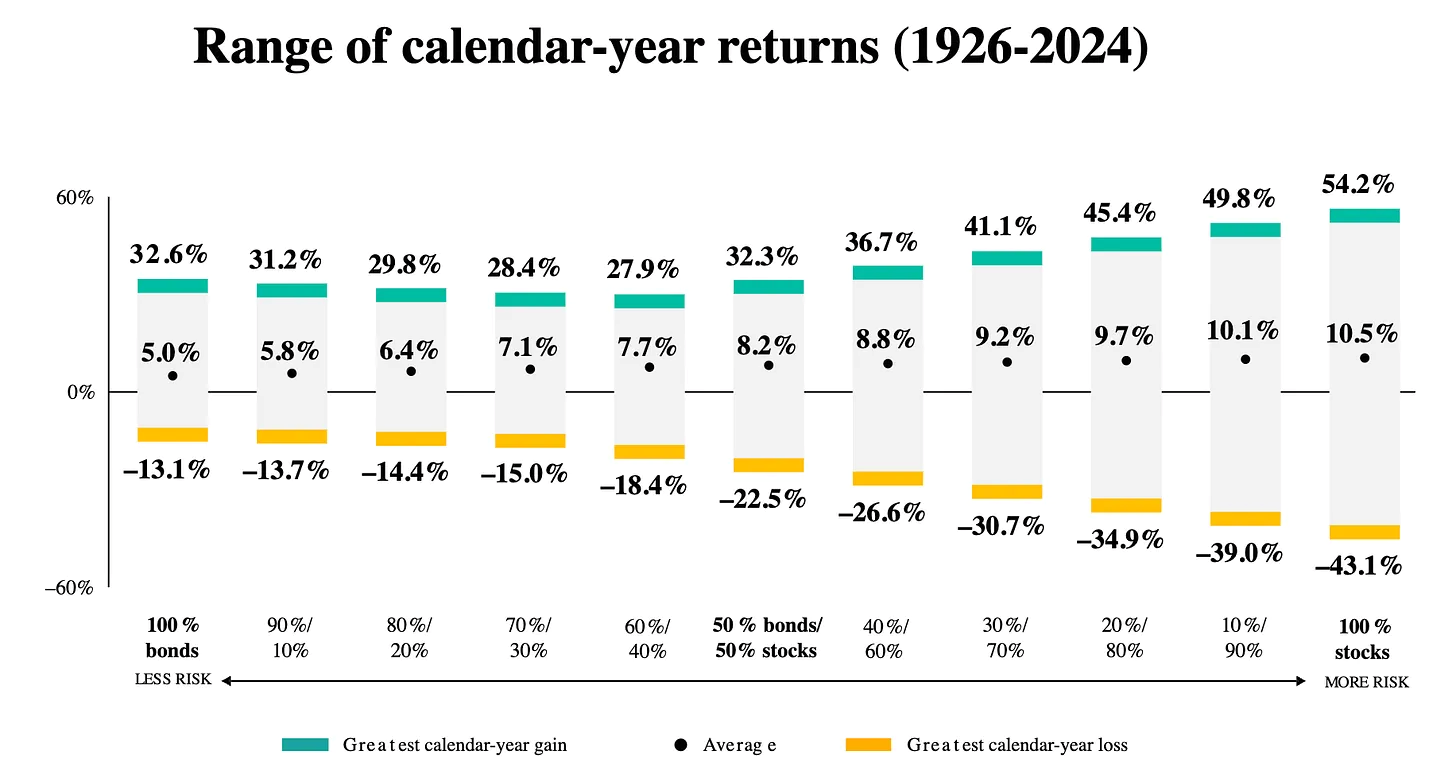

Rebalance for turbulence. I have no idea whatsoever what the stock market will do in 2026. (My assumption is that it will do a bit of everything.) What I can control is how I feel about it. And I can feel pretty sanguine if my portfolio choices reflect a level of risk with which I am fully comfortable. You do you. But know that the idea that you need to be 100% invested in stocks to secure your financial future is simply untrue. You can get where you need to be with much less drama.

Here's a classic chart from Vanguard:

What do you see? That in the long run, your average return from holding only stocks isn’t much different than holding a balanced portfolio…and the ride is much smoother.

Actively (I mean actively) support policies that improve your (and everyone else’s) financial wellbeing. I love the idea of being a low-information voter. To be oblivious to the news cycle and devote myself fully to the NFL would be a dream come true.[1] But that’s not a luxury any of us have right now.

What is happening right now that is affecting your wallet in a tangible way? If you have health insurance, or want to have health insurance in the future, the debate in Congress today on extension of the pandemic bumped-up Affordable Care Act (ACA) premium tax subsidies is vital. Obviously, if you purchase your insurance through the ACA Marketplace, you have already seen the impact. But even if your insurance comes through your employer, the ultimate resolution of the health insurance debate still matters; what happens in the public market ultimately affects private insurance rates. (Here is a great primer on the health insurance market from economist Paul Krugman.)

Whether “your” issue is health insurance or another economic policy such as affordable housing, education or childcare, the point is that now is the time to make your voice heard. If you have elected representation (i.e., you are not a DC resident like me), call them. Repeatedly. Loudly. Especially if they are a Republican and need to be reminded that there are electoral consequences to their actions. Pay attention to all of the “down ballot” races, insisting that candidates specifically address the issues that affect your financial wellness. So much of what affects your livelihood happens at the state and local policy level. And when the opportunities arise, take to the streets.

Not a day too soon, this annus horribulus is coming to a close. Whichever slope of the K-shaped economy you are on, resolve in the new year to, yes, think about your money. But not just your size of your account balances.

(Hey, I’d love to be in touch regularly. My free newsletter contains this blog, as well as other articles written by myself and others. Please consider subscribing by visiting the MoneyByLisa home page.)

[1] Go Birds!